- Sector: Non-Banking Financial Company (NBFC) / Fintech

- Date: May 2024 (Data coverage through FY26 projections)

- Recommendation: ACCUMULATE

- Current Market Price (CMP): ₹ 249

1. Investment Thesis & Summary

Jio Financial Services (JFSL) represents a generational shift in the Indian financial landscape. Emerging from the demerger of Reliance Industries Ltd (RIL), JFSL is positioned as a disruptive, tech-led financial services powerhouse.

Key Pillars of Thesis:

- Capital Powerhouse: Unlike traditional NBFCs, JFSL launched with a massive capital base, primarily driven by its 6.1% treasury stake in RIL, providing it with an unmatched “fortress balance sheet.”

- Ecosystem Advantage: Direct access to RIL’s 450 million+ Jio telecom subscribers and millions of retail customers creates a Customer Acquisition Cost (CAC) advantage that competitors cannot replicate.

- Strategic Global Partnerships: The recent Joint Venture (JV) with Allianz Europe B.V. for General Insurance and the ongoing JV with BlackRock for Asset Management signal a strategy of partnering with global leaders to ensure world-class product delivery.

- Pivot to Operations: FY25-FY26 marks the transition from a holding company to an operational entity, with the ramp-up of consumer lending, device financing, and insurance broking.

2. Business Model & Operations

JFSL operates as a holistic financial services provider through its subsidiaries. Its “Phygital” model combines deep digital integration with the physical footprint of Reliance Retail.

- Lending (Jio Finance Ltd): Focuses on consumer durable loans, personal loans, and merchant financing. The strategy leverages “Jio’s data” to build proprietary credit scoring models.

- Insurance (Jio Insurance Broking): Currently operational in the brokerage space with 30+ insurance partners. The April 2026 announcement of the Allianz JV indicates a move into manufacturing general insurance products.

- Payments & Banking: Through Jio Payments Bank and the JioFinance App, the company aims to capture the UPI and digital wallet ecosystem.

- Asset Management: The BlackRock JV aims to “democratize” investing in India, targeting the massive untapped retail market via digital-first SIP and wealth management solutions.

3. Historical Financial Review

JFSL’s financial profile is currently in an expansionary phase, characterized by significant jumps in revenue as operational segments go live.

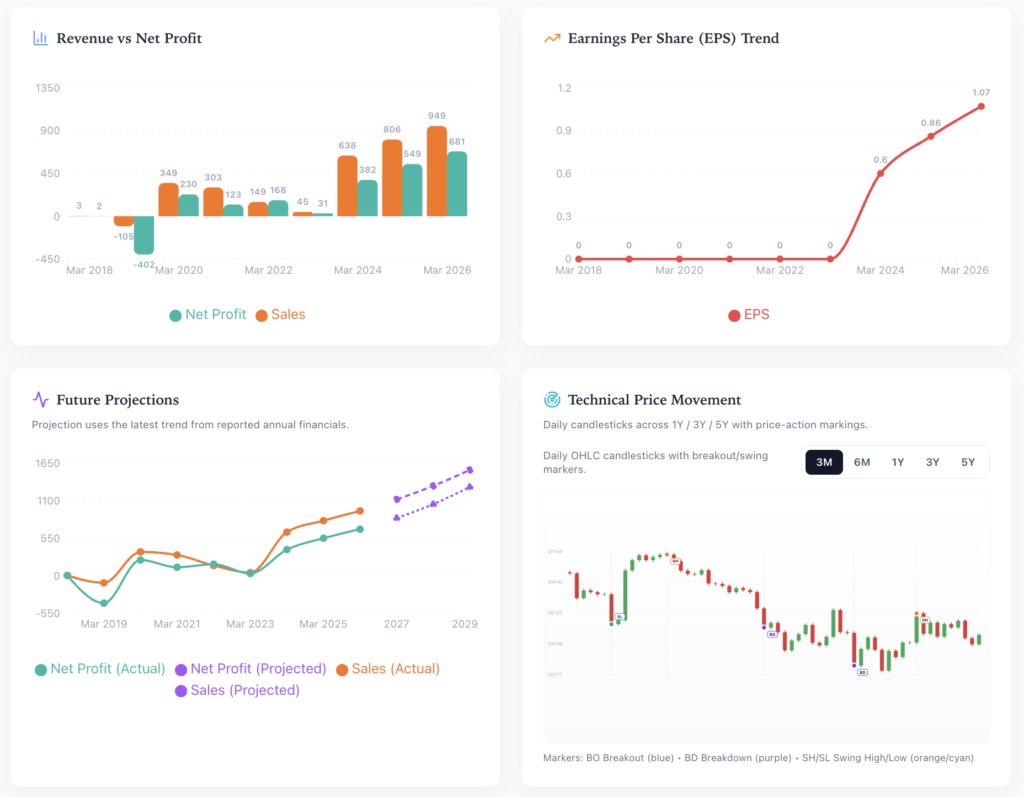

- Revenue Growth: Total “Sales” (Revenue) grew from ₹45 Cr in Mar 2023 to ₹638 Cr in Mar 2024, following the demerger and commencement of operations. FY2026 data shows a further climb to ₹949 Cr.

- Profitability Trends: Net Profit for FY26 reached ₹681 Cr, up from ₹382 Cr in FY24.

- Quarterly Volatility: A significant spike was observed in Sep 2025 (Revenue: ₹520 Cr; Net Profit: ₹456 Cr). This is characteristically attributed to the receipt of dividend income from its RIL shareholdings, which typically occurs in the second quarter of the fiscal year.

- Operational Stability: Recent quarterly runs (Dec 2025 and Mar 2026) show stabilized sales between ₹135 Cr – ₹159 Cr, representing the “base” operational income from interest and fees.

4. Growth Drivers & Catalysts

- General Insurance Entry: The partnership with Allianz Europe B.V. (noted in the April 2026 filing) is a transformative catalyst. Allianz’s global underwriting expertise combined with Jio’s distribution could see JFSL capture significant market share in motor and health insurance within 24 months.

- Asset Management Rollout: The BlackRock JV is expected to launch its first suite of products in late 2024/early 2025, providing a new stream of Fee-Based Income.

- Secured Lending Expansion: Management’s commentary suggests a move into Loans Against Property (LAP) and potentially Home Loans, which will drive AUM (Assets Under Management) growth.

- Device Financing: Aggressive financing schemes for JioPhone and JioAirFiber provide a captive, high-volume lending funnel.

5. Risk Assessment

- Regulatory Scrutiny: As a “Systemically Important” NBFC, JFSL is subject to strict RBI norms. Any tightening of risk weights on unsecured consumer loans (as seen in late 2023) could impact margins.

- Execution Risk: While the capital is available, scaling a high-quality loan book without incurring significant NPAs (Non-Performing Assets) in a competitive market like India is a significant challenge.

- Concentration Risk: A significant portion of the company’s valuation is tied to the RIL stock price. Market volatility in RIL directly impacts JFSL’s book value.

6. Valuation & Price Target

Current Market Price: ₹ 249

Valuing JFSL requires a Sum-of-the-Parts (SOTP) approach, as it acts as both an investment vehicle and an operating NBFC.

- Value of RIL Stake: JFSL holds ~6.1% of RIL. At current market valuations, this holding alone accounts for a significant portion of the market cap, providing a floor to the stock price.

- Operating Business: We value the lending and insurance units at a premium to book value given the zero-debt status and low cost of capital.

- Forward EPS: The jump in EPS from ₹0.60 (Mar 2024) to ₹1.07 (Mar 2026) represents a 78% growth trajectory.

Target Price: Given the strategic Allianz JV and the rollout of the BlackRock partnership, we apply a multiple reflecting JFSL’s status as a “Growth FinTech.”

- 12-Month Price Target: ₹ 315 (Representing a 26.5% upside from CMP of ₹ 249).

7. Management Quality & Governance

Governance is a core strength for JFSL.

- Leadership: Led by banking veteran K.V. Kamath (Chairman), who transformed ICICI Bank, and Hitesh Sethia (CEO), the leadership brings decades of institutional experience.

- Transparency: Recent filings (April 2026) indicate proactive investor engagement, with multiple analyst meets and earnings call transcripts (Regulation 30 LODR), showing a commitment to institutional-grade disclosure.

8. Competitive Positioning

JFSL is uniquely positioned between “Traditional NBFCs” and “Pure-Play Fintechs.”

- Vs. Bajaj Finance: Bajaj remains the gold standard for execution, but JFSL has a lower cost of capital and a larger internal ecosystem (Jio/Retail).

- Vs. Paytm/PhonePe: While fintechs lead in UI/UX, JFSL has a massive balance sheet, allowing it to hold loans on its own books rather than just acting as a distributor.

- Competitive Edge: The Allianz and BlackRock JVs give JFSL institutional credibility that domestic-only players lack, positioning it as a one-stop shop for “All Things Money.”

Disclaimer: This report is for informational purposes only and does not constitute financial advice. Investors should conduct their own due diligence before making investment decisions.

Leave a Reply

You must be logged in to post a comment.