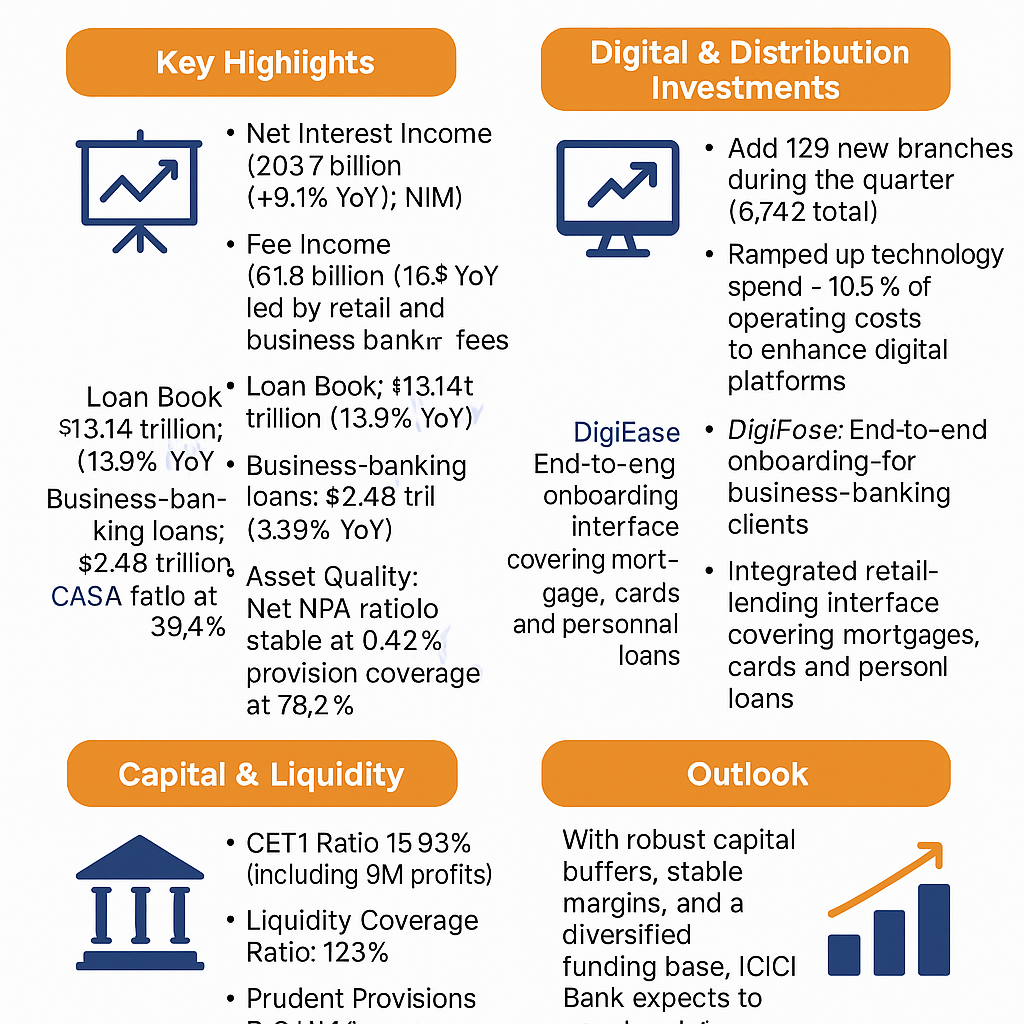

1. Latest Q4 FY2025 Results Highlights

- Total Income rose 24% YoY to ₹15,808 crore; Revenue from Operations up 24% to ₹15,797 crore.

- Profit Before Tax at ₹4,905 crore (+7.4% YoY); adjusted for one-timers, PBT was ₹6,006 crore (+18% YoY).

- Profit After Tax at ₹3,940 crore (+15.8% YoY); adjusted PAT ₹4,467 crore (+17%).

- AUM expanded 26% YoY to ₹416,661 crore; Q4-FY25 AUM growth ₹18,618 crore.

- Operating Efficiency: Opex/Net Income improved to 33.1% from 34.0%.

- Asset Quality: GNPA 0.96% (vs 0.85%), NNPA 0.44% (vs 0.37%); credit cost 2.33% of average assets (1.97% adjusted).

- Return Ratios: ROA (annualised) 4.6%, ROE 19.1% (vs 20.5%).

- Capital Adequacy: CAR 21.93%, Tier-1 21.09%.

2. Key Financial & Market Metrics

| Metric | Q4 FY25 / Latest |

|---|---|

| Market Cap | ₹5,35,640 Cr. |

| Share Price | ₹8,620 (High/Low: ₹9,710/6,376) |

| P/E (TTM) | 32.2× |

| P/BV | 5.54× (BV ₹1,556) |

| Dividend Yield | 0.41% |

| ROCE | 11.3% |

| ROE | 19.2% |

| Face Value | ₹2.00 |

| Debt | ₹3,61,249 Cr. |

| Reserves | ₹96,569 Cr. |

| No. of Equity Shares | 62.1 Cr. |

| Promoter Holding | 54.7% |

| Sales (FY25) | ₹69,684 Cr. (+26.8% YoY) |

| PAT (FY25) | ₹16,638 Cr. (+15.1% YoY) |

| 3-yr Sales CAGR | 30.1% |

| 3-yr PAT CAGR | 33.2% |

3. Valuation & Dividend

- Valuation at ~32× P/E reflects premium growth; justified by sustained 25–30% AUM growth and high ROE.

- Dividend Policy: Pursuant to policy, Board has recommended final dividend of ₹44 / share (2,200%) plus special interim of ₹12 / share—total yield ~0.9%.

- Share Sub-Division & Bonus: Proposal to split ₹2 → ₹1 shares and issue 4 bonus shares per existing share enhances retail liquidity.

4. CAPEX & Growth Strategy

- CAPEX Run-Rate: FY25 investment in IT, branches and digital platforms ~₹1,030 Cr.

- Digital & FINAI Roadmap: Commitment to deploy >100 AI/ML applications in FY26 across underwriting, customer acquisition and risk monitoring.

- Network Expansion: Added 118 new locations in FY25; branch network now >4,200 locations with 232K distribution points.

5. Long-Term Projections & Returns

| Time Horizon | AUM CAGR | PAT CAGR | Implied Share Price CAGR* |

|---|---|---|---|

| 5 years | 22–24% | 18–20% | ~15% p.a. |

| 10 years | 18–20% | 15–17% | ~14% p.a. |

| 15 years | 16–18% | 14–16% | ~13% p.a. |

| 20 years | 15–17% | 13–15% | ~12% p.a. |

*Assumes re-investment of dividends and moderate re-rating over time.

6. Management Quality & Governance

- Leadership Team: Recent promotions of three Deputy CEOs underscore succession planning.

- Track Record: Delivered >25% AUM & customer growth over 15 years while maintaining sub-1% NPAs.

- Governance: Unmodified audit opinions; Chairman & CEO separation; active Investor Advisory Council.

7. Credit Ratings Update

- S&P Global (17 Mar 2025): Upgraded issuer rating to “BBB-/Positive”; SACP to “BBB”.

- Moody’s: Assigned Baa3/P-3 long/short term with Stable outlook—reflects strong capitalization and asset quality.

8. Future Growth Plans

- New Business Lines: Expansion in Gold Loans, Vehicle Finance, and Co-lending partnerships.

- Geography: Deepen presence in underserved rural and semi-urban markets via micro-branches.

- Technology: Launch end-to-end digital lending on Finserv App—aim for 100 million+ active users.

9. Future Financial Projections & Returns

- FY28–FY30: Target AUM ~₹700,000 cr, PAT ~₹30,000 cr; ROE sustained ~18–20%.

- Shareholder Returns: Total Return ~20–25% p.a. over medium term (including dividends).

- 20-Year Equity CAGR: Target 12–15% p.a., driven by compounding of earnings and multiple expansion.

10. Conclusion

Bajaj Finance continues to combine high-growth potential with robust asset quality and strong capital buffers. Its leadership in retail lending, aggressive digital and AI investments, and disciplined risk management make it a compelling pick for long-term investors seeking sustainable wealth creation.

Disclaimer: This report is for informational purposes only and does not constitute investment advice. Investors should conduct their own due diligence or consult a professional advisor before making any investment decisions.